The whole post can be found here on RPubs, as (according to me !) this website provides a nice display for R code, figures and LaTeX formulas. Plus, you can publish directly on Rpubs, simply by using Markdown within RStudio.

Concerning the post content, it’s worth saying that there also a numerical integration error, induced by the calculation of discount factors.

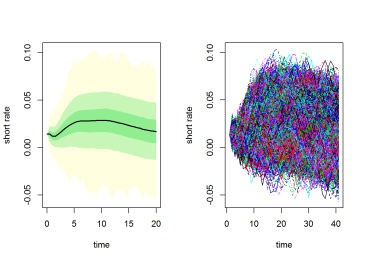

For more ressources on ESGtoolkit, you can read these slides of a talk that I gave last month at Institut de Sciences Financières et d’Assurances (Université Lyon 1), and the package vignette.

Please, cite the package whenever you use it, according to citation(“ESGtoolkit”). And do not hesitate to report bugs or send features request 😉

Hi,

Do you have excel toolkit? If so kindly share.

Regards,

Azmath

LikeLike

Hi, sorry but no Excel tool!

LikeLike

Pingback: Heston model for Options pricing with ESGtoolkit | Thierry Moudiki's blog